Posted on May

8, 2019 by Yves

Smith

The infamous HAMP program,

which the Administration revised so many times on the fly as to give

incompetent and mendacious mortgage servicers air cover for failing to modify

mortgages, at least had a stealth purpose. As Treasury Secretary Timothy

Geithner said to the SIGTARP’s Neil Barofsky, it was to foam the runway for

banks by spreading out foreclosures over time. But that still doesn’t excuse

servicers for their favorite gimmick for not bothering with HAMP applications,

which was to pretend they’d never received them.

But it’s not clear what the

thinking was behind the 2007 Student Loan Forgiveness Program, except to create

better eyewash. The ostensible goal was to give student debt relief for

borrowers who went into socially useful but not>well remunerated lines of

work. But not only were the eligible employers (note employers, not job types)

poorly specified as “public service” which includes some highly paid employees

at not-for-profits, other elements of the program were also drafted badly.

Throw in lousy servicers, revisions to an already confusing program, and

conservative sabotage into the mix, and you’ve created conditions where many

make what they think are the qualifying 120 payments, only to have their

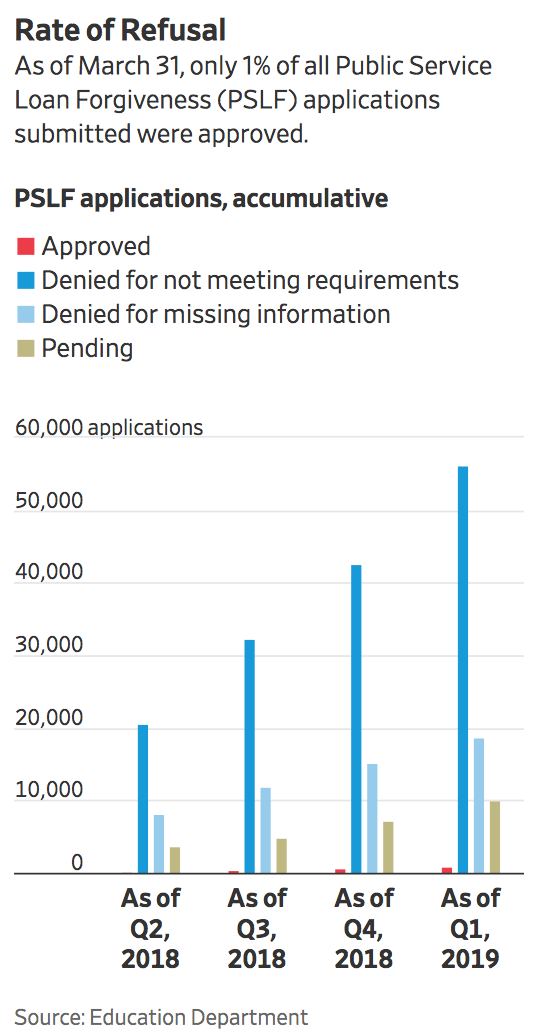

application for forgiveness nixed. Only 1% of 73,000 applicants have gotten

relief.

Admittedly, 25% of the

rejections were due to “missing information,” which means some might eventually

be approved. But as of June 30 last year, 29,000 applications had been reviewed and only 1% were approved,

with 28% needing more information. You’d think by now that if a meaningful

percentage of the then 28% with gaps had had them filled, the proportion being

approved would be rising over time.

The broad outlines of the

abject failure of this scheme aren’t new but the Wall Street Journal provides a

useful overview and update. The program, launched in 2007, created a series of

conditions for eligibility. Per the Journal:

To qualify for forgiveness,

borrowers must work for a government entity or nonprofit, hold a certain type

of loan, enroll in one of several specific repayment plans and make 120 full

and on-time monthly payments, or 10 years’ worth. Falling short on almost any

of these requirements can mean disqualification.

The article describes a litany

of problems. First, only students who had Federal student loans qualified, not

ones with private Federally guaranteed loans. Servicers too often enrolled

borrowers into forgiveness programs for which they did not qualify or gave

incorrect payment amounts.

And even though the Trump

Administration has made its antipathy for the program evident by eliminating it

in its budget announced in March, it’s not as if the Obama Administration did

all that much to make it work. Again from the Journal:

At that point, with the first

borrowers not eligible for forgiveness for seven years, the Obama

administration put off specific steps that would have helped the program run

smoothly. Officials didn’t advertise the program or establish a platform to

guide borrowers through its requirements. They didn’t draw up clear guidance on

which employers should qualify as public-service organizations—now a subject of

litigation. A government investigation last year found that officials didn’t

even produce a guidebook for the servicing company they hired, Fed Loan, to

implement the program.

And measures designed to make

borrowers whole for program screw-ups that did them harm have wound up being

close to moribund:

[Public librarian] Ms.

[Bonnie] Svitavsky hit her first snag in 2013, when she submitted a form to

ensure her employer qualified her for loan forgiveness. It did, but that step

revealed another problem: For the prior 23 months, her servicer, like with so

many other borrowers, had her on a plan known as extended repayment, which

charges standard monthly payments over 25 years. Those payments were now all

ineligible toward her payment count.

The improper payment plan

issue raised particular concern in Washington, where members of Congress, led

by Sen. Elizabeth Warren (D., Mass.), in 2018 created a temporary fund of $700

million to reimburse borrowers who had mistakenly enrolled in ineligible

repayment plans but otherwise qualified. The program has so far granted loan

relief to 442 additional people.

If you generously assume an

average borrower put $10,000 into the extended repayment scheme, only $4

million of the $700 million set aside has been deployed.

Mind you, this isn’t even the

complete litany of things that can or have gone wrong with this program.

Readers have described how they were encourage to consolidate loans to help qualify

for the program…..only to find the new loan wasn’t eligible and had higher

interest charges.

It is distressing to see the

intensity of the hostility in the Wall Street Journal comments section to the

idea giving a break to borrowers. There’s no acknowledgment that students could

have had their employment prospects up ended by the crisis or been misled by

their university about how realistic it would be for them to earn enough to

repay their loans. A few readers did point out the escalating cost of higher

education was the real problem, but the “how could you be so stupid as to get

advanced degrees and then become a librarian?” viewpoint drown it out (never

mind that a Harvard College colleague said the degree she got later in library

science was the most useful education she’d ever gotten; she parlayed that into

a research job at Bain and later a position as head of white label research at

one of the major international equity firms).

I hope large scale debt

forgiveness doesn’t wind up falling into the Maine category of “You can’t get

there from here.” But the experience to date is not encouraging. The fact that

so many hurdles were set up to make sure that only very deserving candidates

could qualify illustrates how few better off individuals are willing to

consider that stagnant real incomes, rising housing, medical and education

costs, and high job instability means that most people go from paycheck to

paycheck and can’t build up a savings buffer. They are one mishap away from

needing to borrow to get by. If they aren’t lucky enough to be able to get the

funds from family or friends, the bank supplied sources range from pricey

(credit cards) to punitive (payday loans). And if you miss a payment due to a

second mishap, it’s well-nigh impossible to get off the treadmill of penalty

rates.

But as long as the well-off

can convince themselves that overburdened borrowers were irresponsible, as

opposed to unlucky, nothing much will change until pitchfork sales go way up.

No comments:

Post a Comment