by Don

Quijones

Chinese corporate defaults

this year through April are 3.4 times the amount last year.

By Don Quijones,

Spain, UK, & Mexico, editor at WOLF STREET.

Since the global financial

crisis, the total value of outstanding corporate bonds has doubled, from

around $37

trillion in 2008 to over $75

trillion today. But the growth has been far from even, with non-financial

debt growing much more rapidly in certain jurisdictions. As the volume and

price of this debt has grown, so too has its riskiness. And that could be a

recipe for disaster, warns Sir

John Cunliffe, deputy governor for financial stability at the Bank of England.

In the US, non-financial debt

is up 40% on the last peak in 2008. Cunliffe expressed even greater caution

concerning emerging markets, where corporate debt as a proportion of the global

debt pile has grown the most over the past 10 years. “Emerging market debt now

accounts for over a quarter of the global total compared to an eighth before

the crisis,” Cunliffe said.

Before the financial crisis,

emerging market companies were issuing a total of $70 billion per year in

bonds, according

to OECD data. That was before the world’s biggest central banks

embarked on the world’s biggest monetary experiment, in which companies the

world over were invited to participate.

By 2016, emerging market

corporations were issuing ten times more money ($711 billion) than before, much

of it in hard foreign currencies (mainly euros, dollars and yen) that will

prove much harder to pay back if their local currency slides, as is happening

in Turkey and Argentina right now. Although bond issuance by emerging market

companies declined by 29% in 2017 and remained around the same level in 2018,

it is still approximately 7.5 times higher than the pre-crisis level.

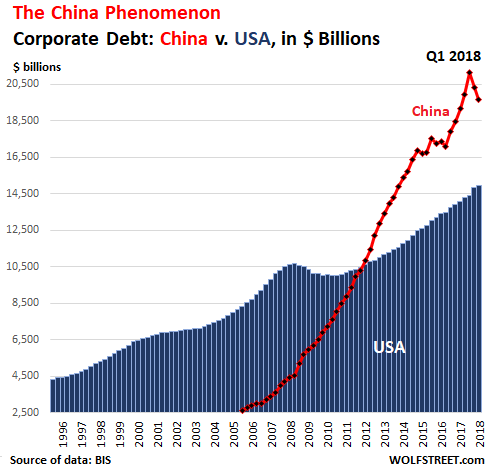

Much of the increase has been

driven by China as it transitioned from

a negligible level of issuance of corporate debt prior to the 2008 crisis to a

record issuance amount of $590 billion in 2016. During that time the number of

Chinese companies issuing bonds soared from

just 68 to a peak of 1,451 and the total amount of corporate debt in China

exploded from $4 trillion to almost $17 trillion, according

to BIS data. By late 2018 it had reached $19.7 trillion.

“There has been a persistent

buildup of private debt to record levels in China,” Cunliffe said. Much of this

increase took place in the direct aftermath of the financial crisis. The

largest increases have been in the corporate sector, mainly in state-owned

enterprises. At last count, China’s corporate debt-to-GDP ratio was 153%,

enough to earn it seventh place on WOLF STREET’s leaderboard

of countries with the most monstrous corporate debt pileups (as a

proportion of GDP), 18 places above the US. This chart compares the rise of

non-financial corporate debt in China and the US:

The rate of growth and level

of debt in China have passed the points where other economies, advanced and

emerging, have experienced sharp corrections in the past, noted Cunliffe citing

research carried out by the Bank of England.

Since early 2017 the Chinese

authorities have been scrambling to deleverage its corporate sector and shrink

its shadow banking system, with a certain degree of success (the hook in the

chart above): corporate debt-to-GDP ratio has fallen in the last two years by

almost 10%. However, in the face of slowing economic growth, the Chinese

government has dialed back some of these reforms as concern rises that a sharp

slowdown in growth would make China’s elevated debt levels even less sustainable.

And if things get seriously

sticky in China’s debt markets, it won’t take long before they’re felt

elsewhere, Cunliffe cautioned:

The Chinese economy is now

pivotal to regional growth and one of the main pillars of world growth and

trade. As well as the economic effects and effects directly through banking

exposures, it is likely that there would be a severe impact on financial market

sentiment, [as happened] in 2015 when a period of sharp correction in domestic

Chinese financial markets sparked a correction in US financial assets.

Problems once again appear to

be on the rise in China. Chinese companies defaulted on 39.2 billion yuan

($5.78 billion) of domestic bonds in the first four months of 2019, 3.4 times

the total for the same period of 2018, according

to data compiled by Bloomberg. For the moment, there’s little sign of

the problems spreading far beyond Chinese borders. In most advanced economies,

as well as quite a few emerging markets (Turkey and Argentina excluded), bond

spreads — the amount charged for risk, be that credit risk or liquidity risk —

are still at or near historically low levels.

But conditions can change on a

dime, as the short-lived drama at the end of 2018 amply demonstrated. Between

mid-October and the end of the year spreads on investment grade bonds widened

by around 50 bps, all on the back of “relatively modest amounts of news,”

Cunliffe noted. “Since then, these moves have fully retraced – spreads at the

start of May were the same as they were in mid-October last year. Bonds in

other currencies and high yield bonds went on a similar round trip.”

When it comes to expectations

about the value of debt, the market can be highly susceptible to changes in

sentiment, meaning a “correction can come very quickly”. As Cunliffe warns,

given the “current compression of risk pricing,” not to mention the sheer

abundance of poor quality, mispriced bonds out there, “such a correction could

be a sharp one.”

No comments:

Post a Comment