December 1, 2017

Last week, the OECD published

its latest World

Economic Outlook. WARNING GRAPHICS OVERLOAD AHEAD!

The OECD’s economists reckon

that “The global economy is now growing at its fastest pace since 2010, with

the upturn becoming increasingly synchronised across countries. This

long-awaited lift to global growth, supported by policy stimulus, is being

accompanied by solid employment gains, a moderate upturn in investment and a

pick-up in trade growth.”

While world economic growth is

accelerating a bit, the OECD reckons that “on a per capita basis, growth will

fall short of pre-crisis norms in the majority of OECD and non-OECD economies.”

So the world economy is still not yet out of the Long Depression that started

in 2009.

The OECD went on: “Whilst

the near-term cyclical improvement is welcome, it remains modest compared with

the standards of past recoveries. Moreover, the prospects for continuing the

global growth up-tick through 2019 and securing the foundations for higher potential

output and more resilient and inclusive growth do not yet appear to be in

place. The lingering effects of prolonged sub-par growth after the financial

crisis are still present in investment, trade, productivity and wage

developments. Some improvement is projected in 2018 and 2019, with firms making

new investments to upgrade their capital stock, but this will not suffice to

fully offset past shortfalls, and thus productivity gains will remain limited.”

The OECD also thinks that much

of the recent pick-up is fictitious, being centred on financial assets and

property. “Financial risks are also rising in advanced economies, with the

extended period of low interest rates encouraging greater risk-taking and

further increases in asset valuations, including in housing markets. Productive

investments that would generate the wherewithal to repay the associated

financial obligations (as well as make good on other commitments to citizens)

appear insufficient.” Indeed, on average, investment spending in 2018-19 is

projected to be around 15% below the level required to ensure the productive

net capital stock rises at the same average annual pace as over 1990-2007.

The OECD concludes that, while

global economic growth will be faster in 2017 and 2018, this will be the

peak. After that, world economic growth will fade and stay well below the

pre-Great Recession average. That’s because global productivity growth

(output per person employed) remains low and the growth in employment is set to

peak. That’s a ‘slow burn’ of slowing economic growth.

But even more worrying for

global capitalism is the prospect of a new economic slump, now that we are some

nine years since the last one. In a chapter

of the World Economic Outlook, the OECD’s economists raise the issue of the

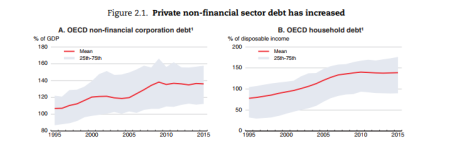

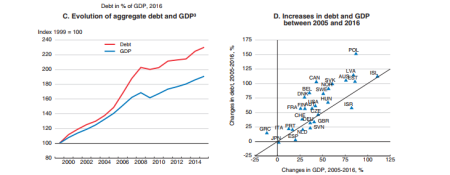

very high levels of debt (both private and public sector) that linger on since

2009. “Despite some deleveraging in recent years, the indebtedness

of households and nonfinancial businesses remains at historically high levels

in many countries, and continues to increase in some.” The debt of

non-financial firms (NFC) rose relative to GDP during the mid-2000s, generally

peaking at the onset of the global financial crisis and remaining stable

thereafter.

After a limited downward

adjustment during the post-crisis period, NFC debt-to-GDP ratios have increased

again since.

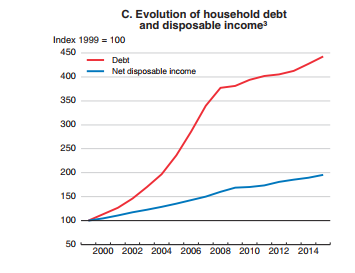

Household debt-to-income

ratios also rose significantly up to 2007 and stabilised thereafter at

historically high levels in most advanced economies. The rise in the

debt-to-income ratio was driven by the acceleration in debt accumulation prior

to the crisis, with subdued household income growth impeding deleveraging

thereafter.

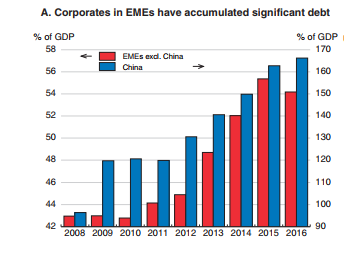

And as I have reported before

in previous posts, non-financial companies (NFC) in the so-called emerging

economies have sharply increased their debt burdens over the last nine years,

so that now, ‘rolling over’ this debt as it matures for repayment amounts to

about half of the gross issuance of international debt securities in

2016. In other words, debt is being issued to repay earlier debt at an

increasing rate.

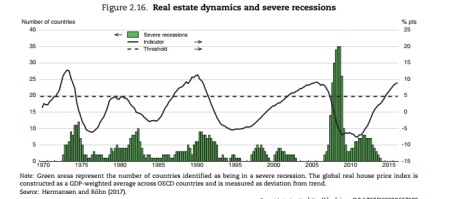

The OECD points out that there

is empirical evidence that high indebtedness increases the risk of severe

recessions. Also, if the prices of ‘fictitious’ assets like property or stocks

get well out of line with the value of productive assets (ie capital

investment), that is another indicator of a coming recession. Currently, there

is no OECD economy in recession (defined as two consecutive quarters of a fall

in GDP), but the global house price index is reaching a peak level over the

trend average that has signalled recessions in the past.

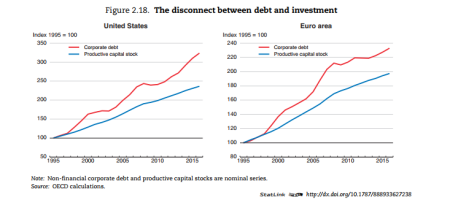

Credit is necessary to

capitalism to overcome the ‘lumpiness’ in capital investment and smooth over

cash liquidity. But as Marx argued, ‘excessive’ credit expansion is a

sign that the profitability of productive investment is falling. As the

OECD puts it: “If borrowing is well used, higher indebtedness contributes to

economic growth by raising productive capacity or augmenting productivity.

However, in many advanced economies, the post-crisis build-up of corporate debt

has not translated into a rise in corporate capital expenditure.”

So the OECD concludes that the

post-crisis combination of rising corporate debt and historically high share

buybacks may suggest that, rather than financing investment, firms took on debt

to return funds to shareholders. This reflects “pessimism about future demand

and economic growth, leading corporations to defer capital spending and return

cash to their shareholders for want of attractive investment opportunities.”

Moreover, firms with a persistently high level of indebtedness and low

profits can become chronically unable to grow and become “zombie” firms. And

zombie “congestion” may thus

reduce potential output growth by hampering the productivity-enhancing

reallocation of resources towards more dynamic higher productivity firms.

So the OECD story is that

world economic growth is picking up and there is little sign of any slump in

production in the immediate future, even if growth may stay well below the

pre-crisis average. But there are risks ahead because the still very high

levels of debt and speculation in financial assets that could come a cropper if

profitability and growth should falter.

This is much the same story

that the IMF told in latest

IMF report on Global Financial Stability that I referred to in

a recent post. As the IMF put it: “Private sector debt service

burdens have increased in several major economies as leverage has risen,

despite declining borrowing costs. Debt servicing pressure could mount further

if leverage continues to grow and could lead to greater credit risk in the

financial system.”

The IMF comments: “While

debt accumulation is not necessarily a problem, one lesson from the global

financial crisis is that excessive debt that creates debt servicing problems

can lead to financial strains. Another lesson is that gross liabilities matter.

In a period of stress, it is unlikely that the whole stock of financial assets

can be sold at current market values— and some assets may be unsellable in illiquid

conditions.” So “if there are adverse shocks, a feedback loop could

develop, which would tighten financial conditions and increase the probability

of default, as happened during the global financial crisis.”

The IMF sums up the

risk. “A continuing build-up in debt loads and overstretched asset

valuations could have global economic repercussions. … a repricing of risks

could lead to a rise in credit spreads and a fall in capital market and housing

prices, derailing the economic recovery and undermining financial stability.”

The IMF posed an even nastier

scenario for the world economy than the OECD by 2020. Yes, the current

‘boom’ phase can carry on. Equity and housing prices can continue to

climb. But this leads to investors to drift beyond their traditional risk

limits as the search for yield intensifies despite increases in policy rates by

central banks. Then there is a ‘Minsky moment’.

There is a bust, with declines

of up to 15 and 9 percent in stock market and house prices, respectively,

starting at the beginning of 2020. Interest rates rise and debt servicing

pressures are revealed as high debt-to-income ratios make borrowers more

vulnerable to shocks. “Underlying vulnerabilities are exposed and the

global recovery is interrupted.” The IMF estimates that the global economy

could have a slump equivalent to about one-third as severe as the global

financial crisis of 2008-9 with global output falling by 1.7 percent from 2020

to 2022, relative to trend growth.

Will the high debt in the

corporate sector globally eventually bring down the house of cards that is

built on fictitious capital and engender a new global slump? When is

credit excessive and financial asset prices a bubble?

The key for me, as

readers of this blog know, is what is happening to the profitability of

capital in the major economies. If profitability is rising, then

corporate investment and economic growth will follow – but also vice

versa. But if profitability and profits are falling, debt accumulated

will become a major burden. Eventually the zombies will start to go

bankrupt, spreading across sectors and a slump will ensue. Financial

prices will quickly collapse toward the real value of their underlying

productive assets.

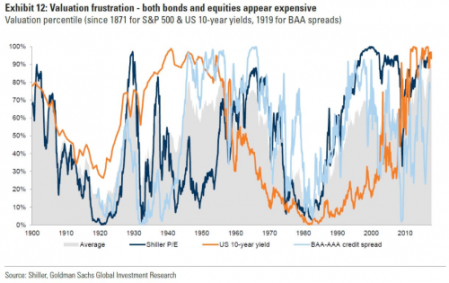

Indeed, according to Goldman

Sachs economists, the prices of financial assets (bonds and stocks) are

currently at their highest against actual earnings since 1900!

What the OECD and IMF reports

show is that if there is a downturn in profitability, the next slump will be

severe, given that private debt (both corporate and household) has not been

‘deleveraged’ in the last nine years – indeed on the contrary. As I

said, in my

paper on debt back in 2012: “Capitalism is now left with a huge debt burden

in both the private and public sector that will take years to deleverage in

order to restore profitability. So, contrary to the some of the

conclusions of mainstream economics, debt (particularly private sector debt) does

matter.”

For now, the world economy is

making a modest recovery from the stagnation that appeared to be setting in

from the end of 2014 to mid-2016. The Eurozone economic area is seeing an

acceleration of growth to its highest rate since the end of the Great

Recession.

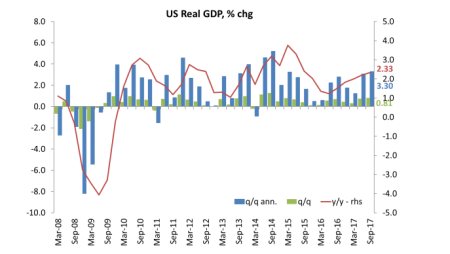

Japan too is picking up, based

on a weak currency that is enabling exports to be sold. And the latest

figures for the US show an annualised rise of 3.3% in third quarter of 2017,

putting year on year growth at 2.3%, still below the rates achieved in 2014 but

much better than in 2016 (1.6%). And the forecast for this current

quarter is for similar.

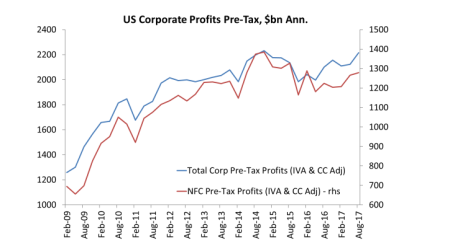

As for corporate profits and

investment, the latest data show that US corporate profits were rising at over

5-7% yoy before tax, although stripping out the mainly fictitious profits of

the financial sector reveals that the mass of profit is still well below the

peak of end-2014.

And as I showed in a recent

post, profitability has fallen since 2014.

IMAGE 11

There is a high

correlation and causality between the movement of profits and productive

investment.

And that is confirmed in the

latest data for the US. As corporate profits have recovered from the

slump of 2015-16, so business investment has made a modest improvement.

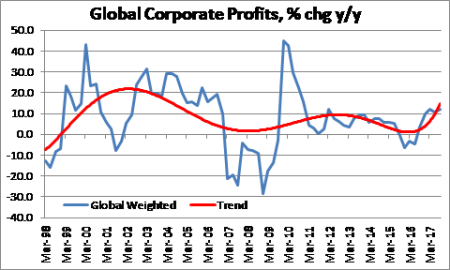

As for global corporate

profits, we don’t have all the data for Q3 2017, but it looks as though it will

continue to be on the up.

So overall, global economic

growth has improved in 2017 and, so far, looks likely to do so in 2018 too.

Corporate profits are rising and that should help corporate

investment. But

profitability of capital remains weak and near post-war lows and

corporate debt has never been higher.

Any sharp upswing in interest

rate costs (and the

US Fed continues to hike) will increase the debt servicing burden. So

if corporate profits should peak and falter in the next year or so, a major

recession will be on the agenda.

No comments:

Post a Comment