Posted on July 8, 2019 by Lambert Strether

By Lambert Strether of

Corrente.

Readers, every so often I

mention the famous New Yorker article about a reporter who accompanies a group

of locals into a swamp to find a bird, thought to be extinct, but whose song

may have been heard. After many many pages, the upshot: They didn’t find the

bird. I’m afraid this post is like that. Among the many unanswered questions

about electric vehicles (EVs) is whether we have enough of the necessary

minerals — lithium, cobalt, nickel — to manufacture their batteries.

We are now at 91 lithium ion

battery megafactories in the pipeline to 2028 #EV

(The vast majority of these

factories are not in the United States[1]) Can we — I suppose as a

species instead of a polity — keep all these factories running? For how long?

Now, I was in Canada for the

Bre-X scandal, “the

most elaborate fraud in the history of mining,” which involved fake

(“salted”) samples of gold; Bre-X had a market capitalization of $4.4 billion

before the fraud was exposed. So I’m not disposed to take reporting on mineral

reserves on faith, and most of the sources I read seemed to be talking their book. (Those in the Naked Capitalism

readership who are minerals fans will correct me on this.) I had hoped to begin

from the material characteristics of lithium, nickel, and gold, from which the

mining technique would follow, and combine that with the location of deposits

to come to some sort of rough estimate of supply, and of the risks involved.

For example, lithium (Li)

is so reactive that it never occurs freely in nature. It dissolves in brine,

so one approach is to look for subsurface brines under dry lake beds, pump the

brine into evaporation ponds, and when the brine is sufficiently concentrated,

extract the lithium and then pump the result back under the lake bed. This is

the approach used for the world’s largest lithium deposits, in the “Lithium Triangle”

(Argentina, Chile and Bolivia). By the Monroe Doctrine, we should be

controlling that piece on the board, but Germany and China seem to be doing the investing. So,

that looks a lot like fracking re-injection to me, an environmental risk, and

there’s geo-political risk as well.

Cobalt (Co),

like lithium and nickel, is only found in chemically combined form, as a

metallic-lustered ore, most often as a by-product of copper and nickel mining

in the Congo, where there are also seams of cobalt close to the surface. As a

result, there are “artisanal miners” — what a phrase — who scour the mine

tailings for shiny cobalt, or dig informal shafts. Here there are political

risks, the Congo being what it is, and public relations risks,

since artisanal miners are often children, and who wants a supply chain (that’s

undeniably) tainted by child labor?

Nickel (Ni) is mined

worldwide (Indonesia, the Philippines, Russia, New Caledonia,

Australia, and Canada, among others. “Nickel mining occurs through extractive metallurgy,

which is a material science that covers various types of ore, the washing

process, concentration and separation, chemical processes and the extraction

process.” So we don’t have artisanal nickel mining, and the environmental

effects are no more than normally bad for “extractive metallurgy”, which is awful. Given the countries where it’s mined, the

political risks seem minimal[2].

But — and this is the longest

windup ever, I feel like Luis Tiant — that approach is simply too complicated,

and doesn’t lead me to the question of supply. So I’m going to move ahead to a

topic-based review of the literature. This is a topic I hope to return to, so I

hope readers will, as it were, provide me with some paths through the swamp, or

even give me a line on the bird.

It’s Not Clear We Have the

Necessary Lithium, Cobalt, and Nickel

There are currently 31.5

million cars on the UK roads, covering 252.5 billion miles per year.

If we wanted to replace all

these with electric vehicles today (assuming they use the most resource-frugal

next-generation batteries), it would take the following:

207,900 tonnes of cobalt –

just under twice the annual global production

264,600 tonnes of lithium

carbonate (LCE) – three quarters the world’s production

at least 7,200 tonnes of

neodymium and dysprosium – nearly the entire world production of neodymium

2,362,500 tonnes of copper –

more than half the world’s production in 2018

Even if we only wanted to ensure an annual supply

of electric vehicles, from 2035 as pledged, the UK would need to annually

import the equivalent of the entire annual cobalt needs of European industry.

For the UK alone. As John

Petersen points out in Seeking

Alpha:

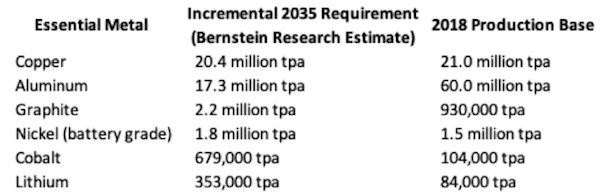

Bernstein Research analyzed

the incremental technology metal requirements for an ~88% transition from ICE

to EV. This table summarizes their conclusions and compares those requirements

with the current global production base for each technology metal:

While aluminum doesn’t present

insurmountable issues and increasing graphite and lithium production from

modest current levels is theoretically possible, doubling

nickel production over a period of 17 years would require herculean effort and

doubling copper production would be almost impossible. Since

cobalt is a byproduct of copper mining in the Congo and nickel mining in other

parts of the world, the only path I’ve seen that has a chance of growing to

meet anticipated demand is sub-sea mining. While extensive work in the 1970s

proved that sub-sea mining was technically feasible, the only commercial

sub-sea operations are diamond mines in offshore Africa.

And we’re on deadline.

Battery Production Is Not

Green

“Like any mining process,

[lithium mining] is invasive, it scars the landscape, it destroys the water

table and it pollutes the earth and the local wells,” said Guillermo Gonzalez,

a lithium battery expert from the University of Chile, in a 2009 interview.

“This isn’t a green solution – it’s not a solution at all.” But lithium may not

be the most problematic ingredient of modern rechargeable batteries…. Unlike

most metals, which are not toxic when they’re pulled from the ground as metal

ores, cobalt is “uniquely terrible,” according to Gleb Yushin, chief technical

officer and founder of battery materials company Sila Nanotechnologies.

I understood about artisanal

mining and child labor, but I didn’t understand that children were handling a

toxic material.

Battery Recycling Isn’t a

Thing

It’s difficult. From Engineering.com:

Whereas lithium batteries are

said to be 95 per cent recyclable, the practice of recycling them is

more easily said than done. Throughout their lifespan, lithium batteries

undergo irreversible damage, meaning that they can’t simply be repurposed.

Instead, they need to be entirely taken apart, the lithium extracted, and then

re-manufactured. But even this is an oversimplification.

Battery manufacturers

incorporate several additives into the electrolyte liquid in the Li-ion

battery. The purpose of these additives is to improve the battery in many ways,

such as by speeding up the manufacturing process, or making the battery

more durable in hot and cold weather. But when manufacturers keep the

battery cocktail a secret, repurposing the precious minerals contained within

becomes difficult and, therefore, expensive.

Moreover, the electrolyte

mixture is the component of the battery that has been known to explode when

handled incorrectly, for instance, if it is subjected to high temperatures. This means that any attempt

at creating a recycling process will need to find a way to ensure that the

batteries are dismantled in a safe manner.

With these difficulties in

mind, it’s not surprising that recycling rates for lithium battery is really

low; only 2 per cent of lithium batteries in Australia are recycled,

with the rest left to rot in landfills. But the problem does not necessarily

come from members of the public carelessly tossing their cracked iPhones into

the trash.

It might be argued that

sustainable recycling infrastructure should come from the car companies—a

process that is still not cost effective compared to market lithium costs, and

therefore provides little incentive. “Recycled lithium is as much as five times

the cost of lithium produced from the least costly brine based process,” Waste-Management-World stated. Even with our best efforts,

recycled lithium is not pure enough to produce batteries, and the material ends

up being used for non-battery purposes.

Recycling will be a big

problem. From CFact:

Most electric vehicles in use

today are yet to reach the end of their cycle. The first all-electric car to be

powered by lithium-ion batteries, the Tesla Roadster, made its market debut in

2008. This means the first generation of electric vehicle batteries have yet to

reach the recycling stage. An estimated 11 million tons of spent lithium-ion batteries will flood our

markets by 2025, without systems in place to handle them.

It doesn’t seem likely that

the externalities of disposing of, let alone recycling, lithium-ion batteries

have gotten much attention in the EV industry, let alone from regulators. I’m

picturing an enormous pile of batteries catching on fire somewhere, but I have

a vivid imagination.

The Prevalance of Magical Thinking

“Sarah Maryssael, Tesla’s

global supply manager for battery metals, told a closed-door Washington

conference of miners, regulators and lawmakers that the automaker sees a

shortage of key EV minerals coming in the near future, according to the

sources.”

Update: Reuters updated their

story to that a Tesla spokesman said: the comments were industry-specific and

referring to the long-term supply challenges that may occur with regards to

these metals.

With EVs at 2% of the market,

I suppose in the short term there are no problems, yes. However:

[Tesla] rarely comments on

supply problems at the mineral level [odd] and when it has in the past, it

mainly brushed off concerns.

That’s partly because cobalt

has been the main concern for many automakers and Tesla’s use in cobalt in its

proprietary [i.e., not recyclable in the general case] battery chemistry is

somewhat limited.

Nickel and copper are the most

common minerals in its batteries, but there are also the most commonly mined.

It’s interesting that they are

now warning that there could be shortages. It’s another indication that the

growth in the industry is going to happen fast in the next few years with so

many different mass market EV programs in the work.

Those

are good problems to have because they indicate that we are going in the right

direction and they are somewhat easily solvable. They just require investments.

“They just require

investments.” And investment is a zero-time task!

Conclusion

I wish I felt I had my arms

round the material completely, but no doubt that will come with future study.

(EV stans, don’t @ me.) Do any of the old codgers in the readership remember

Saturday Night Live’s sketches on Toonces the Driving Cat? This video is

seconds long:

That’s what the EV discourse

reminds me of. For most of the time Toonces was on the road, past

results did indeed predict future performance (“we are going in the right

direction”). Until they didn’t! Was the only requirement “more investment”? No.

Cats like Elon Musk shouldn’t be driving anything!

NOTES

[1] Simon Moores, Managing Director of Benchmark Mineral

Intelligence: “Right now, the US produces 1% of global lithium supply and only

7% of refined lithium chemical supply, while China produces 51%. For cobalt,

the US has zero mining capacity and zero chemicals capacity whilst China

controls 80% of this second stage.” It’s not clear that ramping up domestic

production will be easy, especially on public land. And developing a nickel mine, at

least, can take a decade.

[2] Making this statement from Tesla all the more odd: “Tesla

claims that the nickel in its vehicles is 100% reusable at the end of life, but

refused to disclose to the Guardian where the nickel in its car batteries is

sourced from. In a statement a Tesla spokesperson said suppliers were ‘three or four layers removed from Tesla. It is

obviously quite difficult to have perfect knowledge about everything that happens

this far down in the supply chain, but we’ve worked extremely hard to gather as

much information as possible and to ensure that our standards are being met.'”

If there’s nothing to deny, why all the deniability?

No comments:

Post a Comment