Doug Henwood

In a post yesterday, I

showed how public investment, net of depreciation, in the U.S. is barely above

0, meaning that fresh expenditures on long-lived assets like schools and roads

are running just slightly ahead of the decay of existing infrastructure. You

might think, given neoliberal orthodoxy, that the private sector is taking up

the slack. It isn’t.

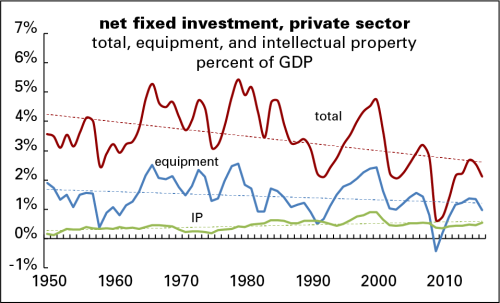

The graph below shows net

private nonresidential fixed investment as a percent of GDP. Net means less

depreciation (the declining monetary value of existing assets over time, as

they wear out and grow obsolete); private means not-government; nonresidential

should be self-explanatory; and fixed means sticking around, as opposed to

inventories, which are considered a form of investment, since businesses

accumulate them for later sale.

Several things stand out

from the graph. First, the declining trendlines on both total investment and

investment in equipment, and the slow rise in intellectual property investment.

Investment in equipment and software—machinery, computers, telecommunications

equipment, etc.—is particularly crucial to long-term productivity growth.

Although the fruits of productivity growth can be distributed in any number of

ways, like higher profits and/or higher wages, the growth in productivity

(meaning the dollar value of an hour of labor) puts an upper limit on income

growth over the long term.

At 2.1% of GDP in 2016,

total net fixed investment is just over half its 1950–2000 average of 3.8%; at

1.0% of GDP, investment in equipment is more than a third below its average

over the same period of 1.6%. (Preliminary figures for 2017 show little change

from 2016 levels.) The recent peak of 2.7% in total investment, set in 2014,

was below the recession lows of 1975 and 1983, and matches the recession low of

2003. In other words, in the best recent year, corporations invested at a rate

matched or exceeded in earlier bad years. Not graphed is investment in

structures—like factories, office buildings, and warehouses—whose trajectory is

very similar to equipment. Its 2016 share of GDP, 0.6%, was a third its 1950–2000

average.

Intellectual property (IP)

investment deserves a few words. It’s been rising as a share of GDP, but it

remains a tiny 0.5%. When it comes to its social benefits, it’s a mixed bag.

About half of it, 47% in 2016, is accounted for by software, both commercial

and custom-made. Some software is useful, like the WordPress code that makes

this blog possible and the Excel and Illustrator code that made the above graph

possible, but some is overpriced and bloaty, like the monstrosities that many

universities run on. A bit less, 42% last year, is research and development

(R&D). Some R&D produces useful products, but an awful lot of it is

just the pursuit of rents from branding and patent scheming. (The leading

culprit here is the pharmaceutical industry, whose basic research is largely

funded by governments and universities; drug companies just come up with

patentable products they can charge a bundle for.) And the remaining 11% is

accounted for by “entertainment, literary, and artistic originals,” which includes Game

of Thrones and Taylor Swift’s recorded oeuvre. While these can

produce pleasure, their contribution to long-term prosperity is hard to

measure.

These low rates of

investment are not driven by corporations’ lack of money; though profits are

down from their peak several years ago, Corporate America is still rolling in

it. But they’re not investing the profits. Instead, they’ve been shipping out

gobs of money to their shareholders—an average of $1.2 trillion a year since

2015. These shareholder transfers take the form of traditional dividends and

stock purchases—purchases of other firms’ stock in takeovers, and of their own

in efforts to boost their prices. If corporations returned to the practices of

the pre-neoliberal era (1952–1983 to be precise), stuffing not half but less

than a fifth of their cash flow in their shareholders’ pockets, that could take

net investment back to its old average. But under today’s model of capitalism,

it’s more important to keep the shareholders happy.

No comments:

Post a Comment